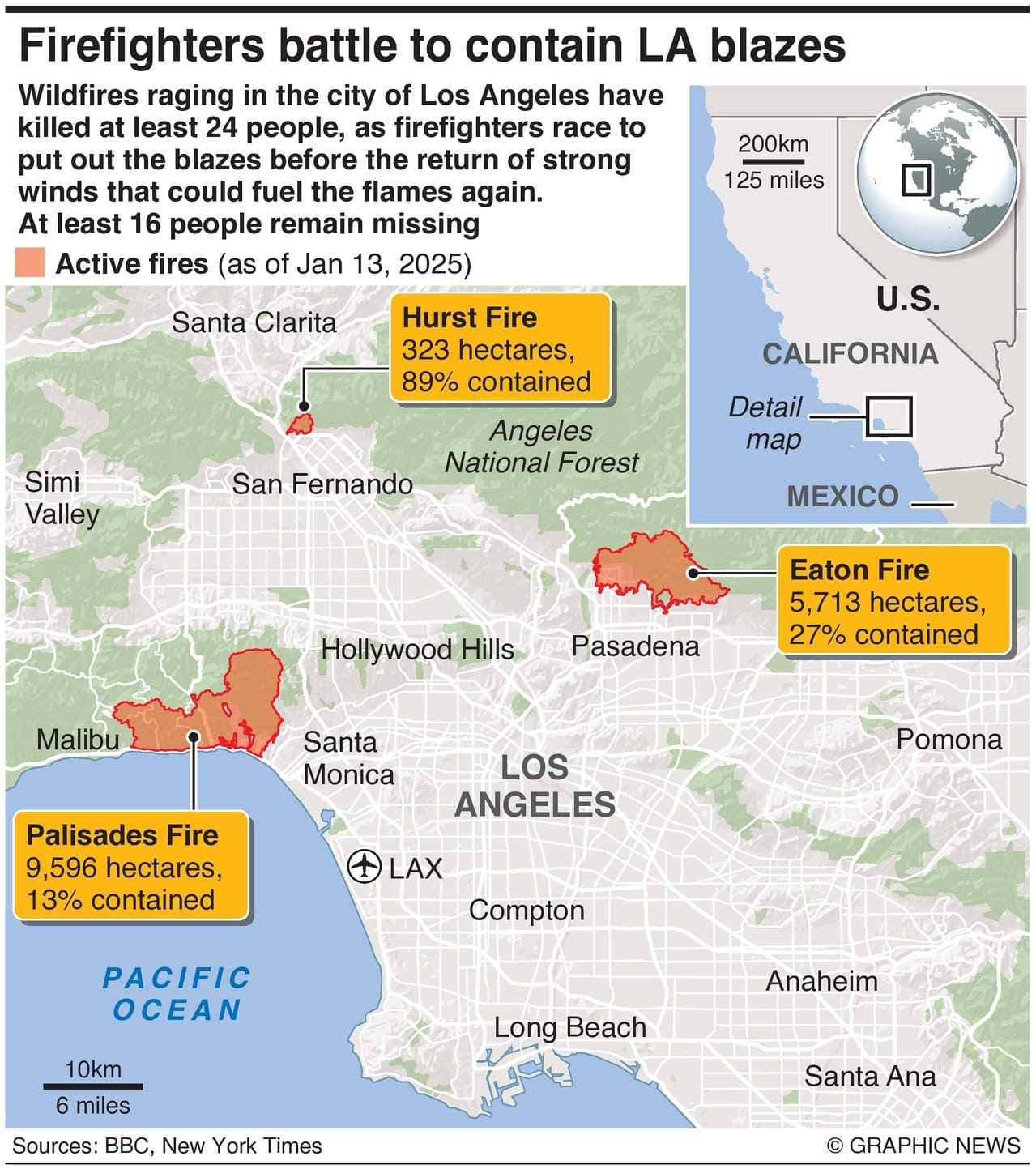

As fires continue to rage in Los Angeles, devouring homes, businesses, and entire neighborhoods, the authorities are rightly focused on saving lives by issuing evacuation orders. The time will come to assess what caused the devastation and what could have been done to prevent it. Then, the painful process of rebuilding will start.

Based on precedent, the American taxpayer will be hit with a hefty bill. Over the years, there has been an expectation that the Federal Emergency Management Agency (FEMA) will step in to help pay for natural disasters. However, the costs to the taxpayer, will not be felt immediately as Washington will borrow the funds and add to the deficit.

A far more crucial concern is what the insurance industry will do. To the extent that they are legally liable, insurers will pitch in and simultaneously begin a nationwide campaign to convince state insurance commissioners to raise rates next year. A family living in flyover country in Kansas and Illinois, far removed from Los Angeles, will be likely hit as the cost of insuring their home goes up.

Unlike automobile or life insurance, the home insurance market in America is regulated at the state level, which means each state has its own set of rules and regulations that dictate how these companies can operate and price their policies. Each state has an insurance department or commission that oversees the insurance industry. These bodies are responsible for ensuring that insurance companies operate fairly and adhere to state laws. They approve policy forms and rates and can investigate complaints against insurers.

In most states, insurance companies must submit proposed rates to the state insurance department for approval before implementing them. This ensures that the rates are not excessively high or unfairly low, which could lead to insolvency. For example, California mandates through Proposition 103 that insurers get rate changes approved by the California Department of Insurance (CDI).

Insurers price their policies based on the perceived risk of insuring a property. They assess the likelihood of claims due to factors like natural disasters, crime rates, and the condition of the home (age, construction materials, etc.). Homes in areas prone to wildfires or hurricanes have higher premiums. Social media posts on X revealed that several Los Angeles-area homeowners lacked insurance protection. The insurers had asked for price increases that CDI did not approve, and when the policies expired, insurers did not offer policy renewals to homeowners. CDI maintains an emergency fund to pay out these claims, but given the extent of the damage, it will likely quickly run out.

The top five home insurance companies in America—State Farm, Allstate, Liberty Mutual, USAA, and Farmers—control nearly 50% of the market and operate in almost every state. These companies have already paid out billions of dollars in claims to cover hurricanes in Texas, Florida, Georgia, and North Carolina last fall. The Los Angeles fires will rack up their claim costs even more. To remedy the health of their books, the companies will request their state overseers for a price increase nationwide, a request that will ultimately be approved. Otherwise, the companies will state that one or more of them could declare bankruptcy.

Over the last 10 years, from 2014 to 2024, the average cost of homeowners insurance in the U.S. has seen a significant rise, from approximately $1,100 in 2014 to an average of about $2,728 per year by 2024 – an increase of roughly 148% over the decade. While every homeowner nationwide pays higher premiums, the Insurance Information Institute says that only about 6% of homeowners actually file a claim. The system effectively redistributes costs, with 94% of homeowners contributing to the coverage needed for the 6% who file claims, often due to living in high-risk areas. This dynamic underscores the broader challenges of balancing equity and risk within the insurance market.

Add the burden of finding a home in a limited-supply environment, higher property taxes as localities reassess property values, and higher maintenance costs as the price of materials and labor goes up, and it is little wonder that new home buyers are scared even to consider entering the market. The lack of supply and higher mortgage costs are severe issues for which there is no quick solution.

Lack of adequate supply: President Biden’s reckless spending during the first three years of his administration drove inflation to record levels. The Federal Reserve Bank raised interest rates from near zero in 2022 to 5.33% in December 2023. Home building and home improvement projects became tremendously expensive as the price of new homes steadily rose, and with few takers, the inventory of new homes fell relative to demand.

An unintended consequence of Bidenflation was that existing homeowners sat tight on their cheap mortgages from years before and refused to list their homes for sale, adding to the housing shortage. Home mortgage rates follow the 10-year Treasury yield and not the Fed Funds rate, which impacts short-term borrowing, such as credit card and auto insurance rates.

At its peak in 2023, a 30-year home loan almost went up to 8%, completely shutting new home buyers out. Existing homeowners enjoying a 30-year loan at 3.5%—locked in during the easy money environment that prevailed much of the decade—would be hard-pressed to sell. Why would a homeowner trade up to pay more each month?

Mortgages are unaffordable for many. Even if a first-time home buyer finds a home to buy, many will find the mortgage payments unaffordable.

The median home in the United States sells for about $430,000. Just a few years ago, a homeowner with a 20% down payment and a 30-year mortgage at a 3.5% interest rate would have paid about $1,450 a month before property taxes, maintenance, and insurance. Today, the 30-year rate is nearly 7%, and the same monthly mortgage payment would be approximately $2,111, a whopping $661 increase.

President-elect Trump understands the real estate business like no other president before him. He should prioritize addressing the housing affordability crisis as part of his MAGA agenda.

TIPP Takes

Geopolitics, Geoeconomics, And More

1. Gaza Deal ‘Can Get Done This Week’: White House – AFP

A Gaza truce and hostage release deal is close and could be finalized in the final week of President Joe Biden’s term, White House National Security Advisor Jake Sullivan said.

“We are close to a deal, and it can get done this week. I’m not making a promise or prediction, but it is there for the taking, and we are going to work to make it happen,” Sullivan told reporters.

2. Ukraine Must Be In Position Of Strength Before Beginning Peace Talks, NATO Chief Says – RFE/RL

NATO chief Mark Rutte told members of the European Parliament that Ukraine is not currently in a position to begin peace talks with Russia.

Ukraine cannot “at this moment negotiate from a position of strength,” Rutte said. “We have to do more to make sure by changing the trajectory of the conflict that they can get to that position of strength.”

3. Germany: Trump’s 5% NATO Demand Too Costly, Scholz Says – D.W.

German Chancellor Olaf Scholz has dismissed demands from President-elect Donald Trump that Germany and other NATO allies increase defense spending to at least 5% of gross domestic product (GDP).

“Five percent would be over €200 billion ($204 billion) per year — the federal budget is not even €500 billion,” Scholz said at a campaign event in the German city of Bielefeld. Germany only reached the current NATO target of 2% of GDP last year, the first time it had done so since the end of the Cold War, and Scholz promised that the country would maintain that level.

4. Chinese Trade Surplus Soars To $1 Trillion Ahead Of Trump Return – Bloomberg News

According to a statement from the customs administration, the surplus jumped to an unprecedented $992 billion in 2024, 21% higher than the previous year.

That was the result of record exports but also the continued weakness of imports, which have been dragged down by sluggish domestic consumption and falling commodity prices. Strong demand from overseas has helped provide growth for a domestic economy weighed down by a yearslong housing crisis.

5. China Mulls Potential Sale Of TikTok U.S. To Musk, Bloomberg News Reports – Al Arabiya

Under one scenario, Musk’s social media platform X would take control of TikTok U.S. and run the business together, the report said, adding that the Chinese officials have yet to reach any firm consensus about how to proceed and their deliberations are still preliminary.

Chinese officials prefer that TikTok remain under the control of parent ByteDance, the report said, adding that the company is contesting the ban with an appeal to the U.S. Supreme Court.

6. Iran Is Changing Its Capital City—Here’s Why – Newsweek

Iran is changing its capital city from Tehran in the north to Makran in the southern coastal region for economic and ecological reasons, according to Persian-language satellite TV station Iran International.

With more than 9 million residents, Tehran has long dealt with overpopulation as well as air pollution, with the capital being one of the worst-polluted cities in the world. The country’s capital has also dealt with what has been referred to as “water bankruptcy,” in addition to electricity and gas shortages. Makran, located in close proximity to the Gulf of Oman and consequently holds various opportunities for improving the country’s trade capabilities, according to the outlet Tehran Times.

7. North Korea Fires Short-Range Missiles Toward Sea Of Japan: South Korea – Kyodo News

North Korea fired several short-range ballistic missiles toward the Sea of Japan on Tuesday, the South Korean military said, in the second round of launches this year.

The latest launch comes around a week before U.S. President-elect Donald Trump takes office on Monday. On Tuesday last week, North Korea’s state-run media reported that the country had successfully launched a new type of intermediate-range hypersonic missile toward a simulated target at sea the previous day.

8. Maha Kumbh Mela: World’s Largest Gathering Begins In India – D.W.

The Hindu festival Maha Kumbh Mela kicked off in Prayagraj in Uttar Pradesh, India. The event takes place once every 12 years in the city, and draws hundreds of millions of people across six weeks.

About 400 million people are expected to attend the six-week festival.

9. Steve Jobs’ Wife ‘Kamala’ Attends Maha Kumbh, To Take A Dip In River Ganga – NDTV

Laurene Powell jobs will stay at the Niranjini Akhara camp till January 15 for Maha Kumbh 2025.

Laurene Powell Jobs or ‘Kamala’, the widow of Apple co-founder Steve Jobs, has arrived in Prayagraj to participate in the Maha Kumbh Mela. A devoted follower of Swami Kailashnand Giri, the Acharya Mahamandleshwar of Niranjini Akhara, Ms Laurene reached the spiritual camp on Saturday night, accompanied by a 40-member team. She will stay in Kumbh and is also planning to take a dip in Ganga.

10. Is Taking Your Required Minimum Distribution (RMD) In January A Good Idea? – The Moltey Fool

Taking your RMDs in January is a particularly useful strategy for those who have RMDs that exceed their expenses, but want to pass on assets to their heirs.

Withdrawing earlier in the year and reinvesting the excess RMD in a taxable brokerage account will provide a very tax-efficient asset to leave to your loved ones. When you pass away, those assets get a step-up in cost basis, effectively wiping out the taxes they’d have to pay on the capital gains. Another reason to take your RMD in January is that you can’t make Roth conversions until after you’ve finished taking your RMD.

10. A Big Social Security Change Just Signed By President Biden Comes With Bad News For Retirees – The Motley Fool

President Joe Biden recently signed the Social Security Fairness Act, legislation that expands benefits for nearly 3 million public-sector workers.

While the Social Security Fairness act is undoubtedly good news for about 3 million public-sector workers, it is also bad news for retired workers and other recipients. The Congression Budget Office estimates the law will accelerate the Old-Age and Survivors Insurance (OASI) Trust Fund depletion by approximately six months, and that it will increase the minimum necessary benefit cut to 26% once the OASI Trust Fund is insolvent.

Related Editorial: Will Our Elected Leaders Ever Fix Social Security’s Broken System?

11. Trump’s Day-One Crypto Executive Order Likely First of Many: Sources – decrypt

President-elect Donald Trump is poised to issue a crypto-related executive order within the opening hours of his second term, sources familiar with the matter told Decrypt—and it’s likely just the first of many to come.

Trump’s first crypto executive order is expected to establish a presidential crypto council, made up of around 20 industry leaders—likely all founders and CEOs, one source said. The order is also likely to instruct the SEC to ditch a rule known as SAB 121 that discourages American banks from holding crypto, two sources said. Congress passed a repeal of SAB 121 last spring, but President Joe Biden vetoed the legislation, leaving the rule in place.

12, Caregivers Face Increasing Physical, Mental Health Risks, Study Says – HealthDay News

More and more adults are stuck in the middle of their families, caring not only for their children, but also for aging parents and other older family members.

The mental and physical health of these “sandwich carers” is more likely to deteriorate over time, a new study published in the journal Public Health says. “It’s crucial that we recognize and support the unique needs of this growing group to ensure their health and resilience,” lead researcher Baowen Xue said.

Republished with permission from TIPP Insights